On June 7, 2017, India joined more than 65 countries in signing the OECD’s Multilateral Instrument to implement tax treaty-related base erosion and profit shifting (BEPS) recommendations. The Instrument – developed under Action 15 of the BEPS project – seeks to transpose BEPS recommendations into over a thousand tax treaties in a “synchronized and efficient manner.” For its part, the Indian Government has decided to cover all of its bilateral tax treaties (93 in total) under the Instrument. The Instrument covers treaty-related minimum standards that were agreed as part of the BEPS package and to which all countries (including India) that are a part of the Inclusive Framework on BEPS have committed to (with some degree of flexibility). India’s position on other Articles of the Instrument is set out below.

Article 3

Article 3 of the Instrument provides that income derived by, or through an entity or arrangement, that is treated as fiscally transparent (wholly or partly) under the law of either contracting state shall be considered to be income of a resident of a contracting state, but only to the extent that the income is treated as the income of a resident of that contracting state. India has chosen to not apply this provision to any of the covered tax agreements and the entitlement of treaty benefits to fiscally transparent entities shall continue to be governed by the existing treaty provisions.

Article 4

India proposes to adopt the tie-breaker mechanism provided under Article 4 of the Instrument (which seeks to give effect to BEPS Action 6 proposal on determining corporate tax residence; see Jonathan Schwarz’s earlier blog on the OECD’s idea behind abandoning POEM). Article 4 states that if a person (other than an individual) is a resident in both contracting states, the competent authorities of the contracting states shall endeavour to determine the residence of the person by mutual agreement, having regard to the place of effective management, place of incorporation, or any other relevant factors. The Article adds that in the absence of such agreement, such person shall not be entitled to any relief or exemption from tax except to the extent and in such manner as may be agreed upon by the competent authorities of the contracting states. It will be interesting to see how India agrees on the definition and application of the POEM test (which is one of the relevant factors to be considered while determining tax residence of companies alongside incorporation etc) given that its guidance on POEM is different from the OECD’s guidance (see my earlier blog where I argued why India should rework its guidance on POEM).

Article 5

India has not adopted any of the ‘Options’ provided for elimination of double taxation under Article 5 of the Instrument.

Article 7

India has chosen to apply the principal purpose test in addition to a simplified limitation of benefits clause to all of its covered tax agreements as provided under Article 7 of the Instrument to prevent treaty abuse (India also has a general anti-avoidance rule, which is applicable starting assessment year April 2018 to “impermissible avoidance arrangement” where the “main purpose” is to obtain a tax benefit). The principal purpose test stipulated in the Instrument is of course wider than the domestic general anti-avoidance rule and it can be argued that there is no need to invoke the general anti-avoidance rule where the principal purpose test is satisfied.

Article 8

India will also adopt the provision relating to dividend transfer transaction under Article 8 of the Instrument (except with its treaty with Portugal as there is a longer holding period), which requires a minimum holding period to be met before certain reduced rates on dividends are available. The Article has little impact as India imposes a dividend distribution tax on profits.

Article 9

India has chosen to adopt Article 9 of the Instrument, which provides for rules for taxation of capital gains arising from alienation of shares or interests of entities deriving their value from immovable property. As per the Article, the source state will get taxing right if the value threshold is met any time within 365 days preceding the date of transfer (also applicable to interest in partnership or trusts).

Articles 10 and 11

India will adopt the anti-abuse rule for permanent establishments situated in third jurisdictions stipulated in Article 10 of the Instrument, and the provision on application of tax agreements to restrict a party’s right to tax its own residents stipulated in Article 11 of the Instrument.

Articles 12, 13 and 14

India has chosen to adopt the provisions contained in the Instrument with respect to artificial avoidance of permanent establishment status through commissionaire arrangements and similar strategies (Article 12); artificial avoidance of permanent establishment status through the specific activity exemptions (Article 13, India has chosen ‘Option A’); and provisions on splitting-up of contracts (Article 14).

Article 16

India has reserved its right to not apply the provision relating to mutual agreement procedure (MAP) to its covered tax agreements in the entirety as provided under Article 16 of the Instrument, that it, it has opted for bilateral notification or consultation process (which is a minimum standard) and will not allow taxpayers to approach competent authority of either of the contracting jurisdiction. As expected, India has expressed reservations to adopt mandatory binding arbitration (see my earlier blog where I argued why India should adopt MAP arbitration).

Article 17

India has expressed reservation to adopt corresponding adjustments provision in related-party transactions for those covered tax agreements that already have provisions for corresponding adjustments. Article 17 of the Instrument provides for corresponding adjustments to be made by contracting states to eliminate double taxation. In India, adoption of this provision will pave way for settlement of transfer pricing disputes via MAP and bilateral advance pricing agreements.

Way forward

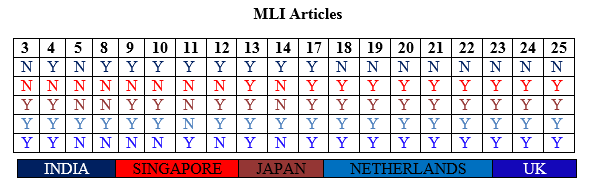

Some of India’s key treaty partners include Germany and Mauritius (who have not notified their tax treaties with India), Japan, the Netherlands, Singapore, the UK, and the US (not a signatory to the Instrument). The table below compares India’s position under the Instrument as against Japan, the Netherlands, Singapore, and the UK.

The position of countries, of course, is provisional and they are entitled to amend their positions anytime before ratification. Contracting parties are also allowed to opt in with respect to optional provisions or withdraw reservations even after ratification. The future recourse is to wait and see until the first round of modifications to covered tax treaties, which will become effective in the course of 2018.

________________________

To make sure you do not miss out on regular updates from the Kluwer International Tax Blog, please subscribe here.