On 23 May the OECD published a Public Discussion Draft on Implementation Guidance on Hard-to-Value intangibles (HTVIs). Comments are due by 30 June 2017, so hurry.

1. Introduction

All guidance by the CFA and the opportunity to comment is appreciated, especially on a major topic like intangibles. That being said, I think that this paper can do more in terms of guidance on the new chapter 6.D.4 of the Transfer Pricing Guidelines (HTVIs). One needs to start with the text of chapter 6.D.4 to identify the missing guidance. I see the following issues:

- I have difficulty in understanding the relation between intangibles (including HTVIs) and profit potential referred to in chapter 9. Is profit potential an HTVI (unlikely considering the language of chapter 9); is profit potential an attribute of an HTVI; or is profit potential something besides tangibles and intangibles (e.g. the difference between the going concern value of an enterprise and sum of its total tangibles and intangibles). If the latter is the case, it will be good to know if the principles of § 6.188 – 6.194 apply as well. (actually, after BEPS, the consolidation of the Transfer pricing guidelines in general would increase its ease of use, e.g. also connecting the dots between chapter V, annex I and II, and chapters I.D.1, III and VII.D.)

- There is an ambiguous sentence in §6.188: “Such presumptive evidence may be subject to rebuttal as stated in paragraphs 6.193 and 6.194, if it can be demonstrated that it does not affect the accurate determination of the arm’s length price.” where the second “it” either refers to “presumptive evidence” or “it” refers to the “rebuttal”. I find it difficult to understand either alternative. I assume it is should read (summarised) “presumptive evidence can be rebutted if the presumptive evidence does not affect the determination of the arm’s length price.” but I still do not know what it means. Does it mean that if the presumptive evidence does affect the arm’s length price, then rebuttal is not possible? If yes, does that then mean that this sentence constitutes a threshold for 6.193 (not logical considering the fact that the thought process behind chapter 6.D.4 seems to be linear and then a throw-back from 6.193 to 6.188 makes no sense); if no, then why the “if”, which makes the sentence conditional?

- There is the question whether the possibilities of the rebuttal of the presumptive evidence is limited to the examples given in 6.193 (which the current wording of 6.188 and 6.193 imply), and if so, why. It seems fair as a matter of principle that presumptive evidence should be allowed to be rebutted in any possible way, as long as the rebuttal is credible.

- There is the unexplained difference in base of the 20% exemptions under 6.193.iii and iv: under iii the significant difference does not move the compensation more than 20% and iv the projected commercial outcomes may not vary more than 20% from the actual outcomes. I am not sure if this makes a big difference in numerical outcomes, but I do think that the difference in wording can generate confusion.

- To what extent are taxpayers themselves allowed to apply the ex post presumptive evidence to justify spontaneous adjustments to previously made transfers of HTVI’s. After all honest mistakes do happen. Also are the thresholds for change different from those applicable to tax authorities?

2. What does chapter 6.D.4 say

Definition of HTVI’s

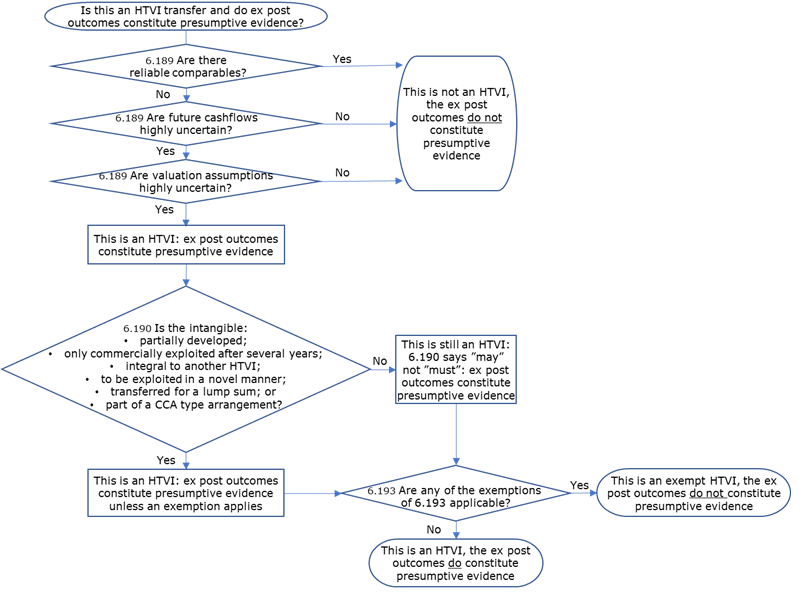

Taken together, HTVI’s under § 6.188 – 6.193 are supposed to look something like this.

In short, if there are no reliable comparables and the future cash flows and valuation assumptions are highly uncertain, ex post outcomes always constitute presumptive evidence UNLESS the intangible is transferred against a royalty AND the intangible is fully developed, can be commercially exploited within 1 or 2 years, is not integral to another HTVI, will not be exploited in a novel manner AND is not developed or used under a CCA type arrangement. Unless we drastically restrict the meaning of “unique” in “unique intangibles”, this makes the vast majority of intangibles, HTVI’s.

It will help if the OECD guidance can explain how HTVI’s are different from other transactions where there are no comparables, no reliable future discount cash flow calculations or reliable future assumptions.

The difference between using ex post outcomes as presumptive evidence and hindsight

According to § 6.188, last sentence, using ex post outcomes as presumptive evidence differs from hindsight in that hindsight also uses ex post outcomes, but does not consider whether the information on which the ex post results are based could or should reasonably have been known and considered by the associated enterprises at the time the transaction was entered into. This is a useful differentiation. It will help taxpayers and tax authorities alike, if it is clearly made applicable to the rest of the guidelines as well.

1. The HTVI Guidance paper

Now that we recapitulated what chapter 6.4.D is about, it makes sense to see whether the paper provides any guidance on the issues described above. It does not. Instead it adds/expands the existing confusion and uncertainties.

The paper has an introductory chapter summarizing the difficulties tax authorities have in determining the arm’s length price of HTVI’s; it discusses timing issues; and it urges tax authorities to identify HTVI transfers and audit them as soon as possible. Finally, the guidance discusses 3 and a half examples:

- one illustrating an appropriate adjustment where the exploitation phase commences much faster than the contracting parties priced them for (example 1A), but where the compensation adjustment is less than 20% of the compensation, as described in § 6.193.iii (example 1B);

- one illustrating an appropriate adjustment where the commercial exploitation results are higher than assumed when the contracting parties priced the transfer and where the adjustment can take the form of a subsequent contingency payment; and

- one involving a recurring royalty that should be adjusted in retrospect, but where double taxation may arise because the payee country’s statutes of limitation may be shorter than the payor country’s.

The worrisome aspect of the issued guidance is that besides not addressing the issues identified here above, it adds 2 new concerns for taxpayers. First, example 1.B stops with merrily mentioning that even if the ex post presumptive evidence procedure does not apply, the rest of the guidelines still do. Though I cannot condemn it outright, I have mixed feelings about having a rule, providing a safe harbor to that rule, and then taking the safe harbor away again. It would be nice if this conclusion that the rest of the guidelines still apply can be accompanied by the clear statement that no other form of using ex post outcomes being presumptive evidence, nor hindsight, are available to tax authorities in such a case.

Second, example 3 seems rather complacent about the double taxation arising for taxpayers out of the adjusting authority having a longer statute of limitation than the corresponding adjusting authority. So much so that it makes no mention of article 25, second paragraph, last sentence, which reads “Any agreement reached shall be implemented notwithstanding any time limits in the domestic law of the Contracting States.” with an accompanying commentary in paragraph 39 to the article reading: “The purpose of the last sentence of paragraph 2 is to enable countries with time limits relating to adjustments of assessments and tax refunds in their domestic law to give effect to an agreement despite such time limits.”

2. Concluding wish list

So all in all, I have the following wish list regarding this paper:

- Please explain the relationship between HTVIs and profit potential in particular, or better still the relationship between intangibles and profit potential.

- Please explain the ambigious sentence in § 6.188 and confirm that chapter 6.D is a linear process.

- Please confirm that the rebuttal possibilities against presumptive evidence extend beyond §6.193.

- Please confirm that taxpayers can apply chapter 6.D as well for spontaneous (two-sided) adjustments.

- Please confirm the scope of the use ex post outcomes as presumptive evidence and the differentiation between presumptive evidence and hindsight. Do these only apply to chapter 6.D, or to chapter 9 as well, or to the whole guidelines? Also please reference this in example 1.b of the paper.

- Please be more pro-active on preventing the possible double taxation arising under example 3.

________________________

To make sure you do not miss out on regular updates from the Kluwer International Tax Blog, please subscribe here.

Thank you for this post, it will help me get my juice flowing to submit some comments on HTVI. Plopped this onto LinkedIn and Twitter.

Good post. Thanks.